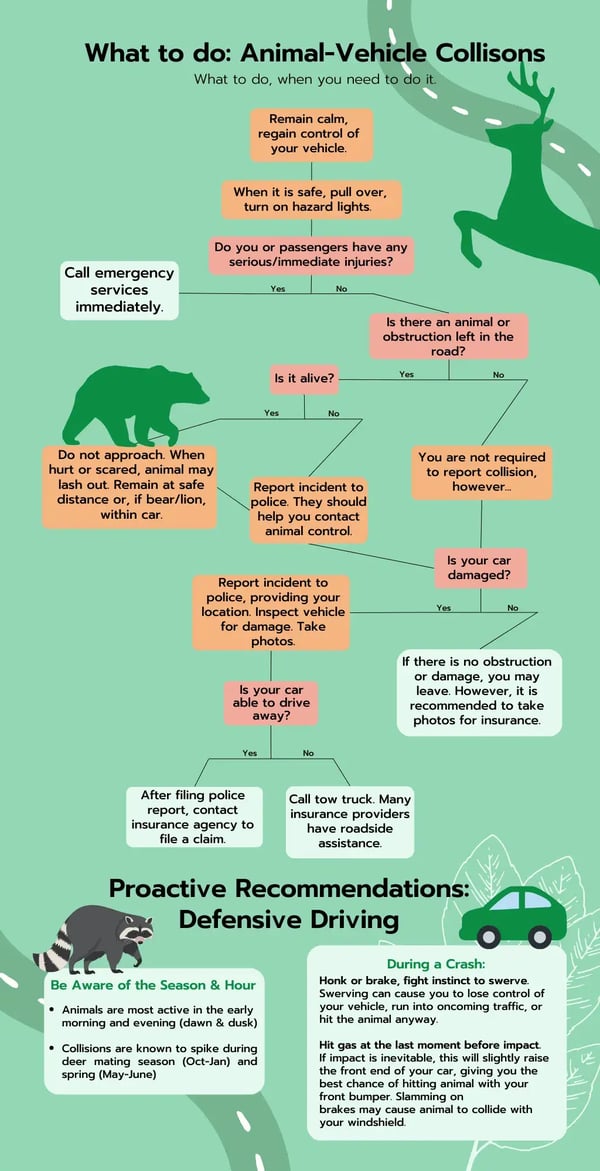

How Hitting a Deer Affects Your Insurance: What You Need to Know

Will my insurance go up after hitting a deer?

When you hit a deer, the aftermath can be both stressful and costly. One of the most pressing concerns for many drivers is whether their insurance premiums will increase as a result of the accident. The answer to this question largely depends on several factors, including your insurance provider, the specifics of your policy, and your driving history.

Factors Influencing Insurance Premium Increases:

- Type of Coverage: If you have comprehensive coverage, which typically includes animal collisions, your insurance may cover the damages without significantly impacting your premium.

- Claim History: If this incident is your first claim, some insurers may not raise your rates. However, frequent claims can lead to higher premiums.

- State Regulations: Insurance laws vary by state. In some regions, hitting a deer may not be considered an at-fault accident, which could help keep your rates stable.

- Insurance Company Policies: Each insurer has its own policies regarding accidents involving wildlife. Some may treat deer collisions differently than other types of accidents.

Additionally, it’s essential to consider how your driving record plays a role in determining your insurance rates. If you have a clean record and this is your first incident, insurers may view you as a lower-risk driver, which could mitigate any potential increase in your premium. On the other hand, if you have multiple accidents or claims on your record, hitting a deer could lead to a more significant rise in your rates.

Ultimately, it’s advisable to contact your insurance provider directly after such an incident. They can provide specific information based on your policy and circumstances, helping you understand the potential financial impact of hitting a deer on your insurance premiums.

Should I file an insurance claim if I hit a deer?

If you find yourself in the unfortunate situation of hitting a deer, one of the first questions that may arise is whether you should file an insurance claim. The decision can depend on several factors, including the extent of the damage to your vehicle, your deductible, and the type of coverage you have. Understanding these aspects can help you make an informed choice.

Assess the Damage: Before deciding to file a claim, it’s crucial to assess the damage to your vehicle. If the damage is minimal, you might consider paying for the repairs out of pocket. However, if the damage is significant, filing a claim could be necessary. Common signs of severe damage include:

- Cracked or broken headlights

- Dented bumpers

- Damaged fenders or hood

- Fluid leaks

Your Deductible: Another critical factor to consider is your insurance deductible. If the cost of repairs is less than your deductible, it may not make sense to file a claim. For instance, if your deductible is $1,000 and the repair costs amount to $800, you would be better off covering the expenses yourself. On the other hand, if the repairs exceed your deductible, filing a claim could help you recover the costs.

Type of Coverage: The type of auto insurance coverage you have can also influence your decision. Comprehensive coverage typically includes incidents involving deer, whereas liability insurance does not cover damage to your vehicle. If you have comprehensive coverage, filing a claim may be a viable option to mitigate your financial loss. However, keep in mind that filing a claim could potentially impact your insurance premiums in the future.

Is hitting a deer with your car considered an act of God?

When discussing the legal implications of hitting a deer with your vehicle, the term "act of God" often arises. An "act of God" refers to natural events that are beyond human control, such as floods, earthquakes, or severe weather conditions. However, when it comes to wildlife collisions, the classification can be more nuanced. While deer are indeed part of nature, the circumstances surrounding a collision can determine if it fits the definition of an act of God.

In many jurisdictions, hitting a deer is generally not classified as an act of God for insurance purposes. This is primarily because, unlike unpredictable natural disasters, deer can be anticipated in certain areas, particularly in rural or suburban regions where wildlife is common. Drivers are often warned of potential deer crossings through signage, and many states have established peak seasons for deer movement, particularly during mating season in the fall. As such, the responsibility may lie with the driver to remain vigilant and exercise caution.

Factors that may influence the classification include:

- Location: Areas known for high deer populations may not support an act of God argument.

- Time of day: Deer are more active at dawn and dusk, which could affect a drivers ability to avoid a collision.

- Driver behavior: Distracted driving or speeding can complicate claims related to deer collisions.

Ultimately, while hitting a deer may seem like an unavoidable accident, the classification as an act of God can vary by state and specific circumstances. Its essential for drivers to understand their insurance policies and local laws to navigate the aftermath of such incidents effectively. Understanding these nuances can help in determining liability and coverage options in the event of a deer-related accident.

Will rates go up if you hit a deer?

When you hit a deer with your vehicle, one of the primary concerns that may arise is whether this incident will lead to an increase in your insurance rates. The answer can vary based on several factors, including your insurance provider, your policy type, and your driving history. Generally, hitting a deer is classified as a collision claim, which can potentially impact your premiums.

Factors Influencing Rate Increases:

- Your Insurance Provider: Different insurance companies have varying policies regarding animal collisions. Some may not raise your rates for a first-time claim involving a deer, while others might.

- Claims History: If you have a history of multiple claims, even if they are not all deer-related, your insurance company may view you as a higher risk, leading to increased rates.

- State Regulations: Some states have laws that protect drivers from rate increases due to animal-related accidents, so its essential to check local regulations.

Its also worth noting that if you have comprehensive coverage, which typically covers damage from animal collisions, you might face less of a rate hike compared to collision coverage claims. However, if you opt to file a claim, even with comprehensive coverage, you could still see an increase in your premiums depending on your insurers policies.

Additionally, if you choose not to file a claim and pay for the damages out of pocket, your rates are unlikely to be affected. This decision can be beneficial if you want to maintain your current premium level and avoid potential rate increases in the future. Always consult with your insurance agent to understand the specific implications of hitting a deer on your insurance rates.

Leave a Reply

You must be logged in to post a comment.